Reflections on Chinese Companies’ Global Investments in the Hydropower Sector Between 2006-2017

Introduction

The Chinese government has prioritized the hydropower sector since the 1999 “Going Out” strategy. During this period, Chinese companies and Chinese banks have become the biggest builders and financiers in global dam building. Indeed, just one Chinese company, PowerChina Resources, is estimated to have as much as a 50% share of the international hydropower construction market (from 2016 PowerChina Corporate Social Responsibility Report).

International Rivers tracks all Chinese hydropower companies’ investments throughout the world. Our latest revision of the China Global Dams Database was completed in September 2017 and is now available for public use (kindly attribute to International Rivers). This is the only such comprehensive compilation of information. Books and online resources in many countries and languages have referenced previous editions of the database, including China's Rising Influence in Developing Asia; Chinese Encounters in Southeast Asia: How People, Money and Ideas from China are Changing a Region; Sudan Looks East: China, India & the Politics of Asian Alternatives (online resources include E-International Relations, AidData, Global CCS Institute and Forbes). We hope that this tool will continue to help individuals and organizations researching topics such as how many dams are being planned or constructed in particular countries or regions; which Chinese companies are funding which dams; and how much money is being spent.

This new edition of the China Global Dams Database is more user-friendly. It is easier to search, more consolidated and better organized. The analysis of Chinese hydropower companies’ investment trends over the past ten years is intended to complement and contextualize information in the database.

General Trends

The China Global Dams Database includes 323 projects. The analysis below is based exclusively on the 266 hydropower projects undertaken in 64 countries and at various stages of development; it does not include dams built for irrigation or other purposes. The hydropower projects analyzed follow different models: Build-Operate-Transfer (BOT); Engineering, Procurement & Construction (EPC); or construction contracts for part of the hydropower project.

Chinese involvement in hydropower contracts overseas peaked, by project number and megawatt (MW) capacity, between 2007 – 2011 (Figure 1). This peak appears to be primarily due to contracts signed in Burma and Laos in 2007, and additional large-scale contracts in Burma and Cambodia in 2010. In 2016 and 2017, the capacity (in megawatts) of signed projects increased again, though not the number of projects.

Types of Contracts

There are two main contract types for Chinese hydropower companies:

• Engineering, Procurement and Construction

• Build-Operate-Transfer.

During the early years, Chinese hydropower companies building outside of China typically acted as contractors. Nowadays, Chinese hydropower companies can be responsible for all Engineering, Procurement and Construction (EPC) contracts, or just specific aspects of the hydropower project, such as constructing civil or hydraulic works, or supplying electrical equipment. Under the EPC model, governments or the utilities assume the financing to carry out the preliminary studies, publish pre-qualification documents, and are responsible for the technical, legal and other guarantees, as well as the investment or plant operation.

Today, many Chinese hydropower companies are also signing contracts to Build-Operate-Transfer (BOT). The BOT arrangement combines public and private resources to make large-scale infrastructure viable. The company finances, designs, builds and provides human resources for construction and operation, in exchange for the operating rights over a period of time, typically 20-30 years. The number of years varies and is usually set so that the company can recover investment costs before handing back ownership to the government.

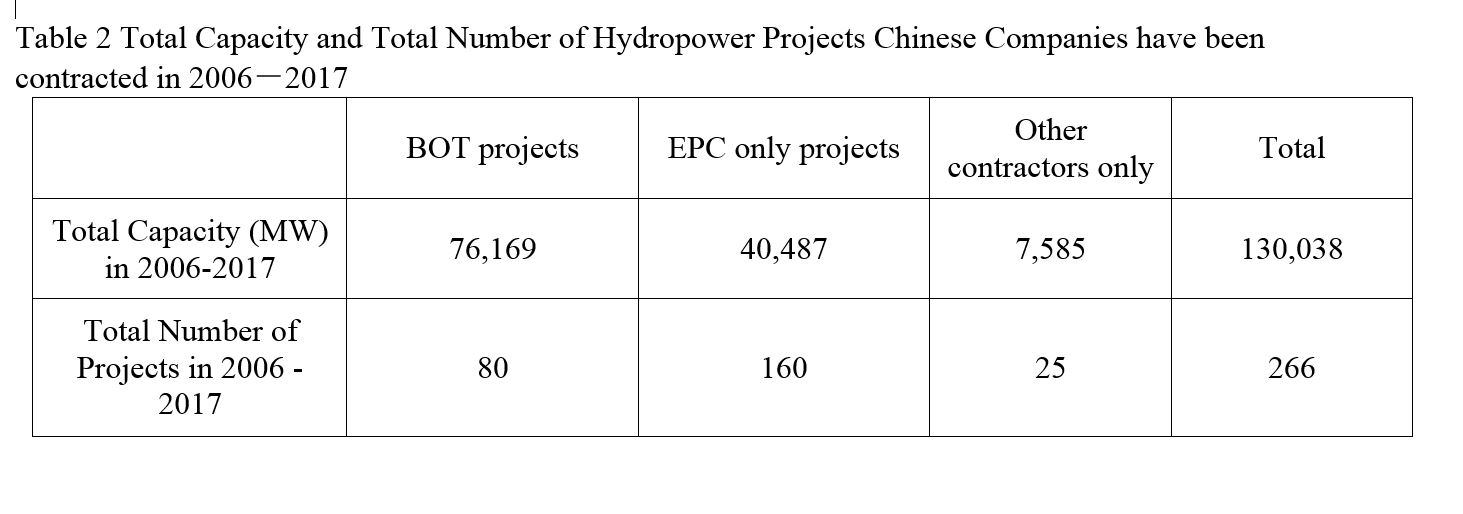

Over the past ten years, Chinese companies have won more EPC than BOT contracts. Chinese EPC contractors are currently most active in Africa. However, though the Chinese companies have signed fewer BOT projects, they have been higher in hydropower capacity by megawatts (Table 2). When Chinese companies sign BOT contracts, they usually hire Chinese companies as construction contractors.

Chinese hydropower companies have been very interested in the BOT model: They’ve explored BOT opportunities in Burma, Cambodia, Laos, Nepal and Pakistan. However, they have faced great challenges in developing BOT projects. Due to the operational nature of BOT models, the size of the projects, and where the projects are located, Chinese companies face big challenges managing the environmental and social impacts associated with BOT projects. More than half of the BOT projects signed by Chinese companies haven’t even begun construction yet. China Three Gorges, Datang and PowerChina Resources are the three most active Chinese BOT developers. Huaneng is trying to expand its market share in Southeast Asia, and has Shweli 2 in Burma and potentially Sambor in Cambodia in the pipeline. China Power Investment Corporation has been idle, with no changes in status for eight projects (with a capacity of 18,259 MW) in Burma, which were signed in 2007 and 2011.

Geographic Trends

Among the 64 countries where Chinese companies have been active over the past ten years, the biggest investments by capacity have occurred in Burma, Pakistan, Laos and Cambodia. Macedonia ranks highly, because of a cascade of 12 small dams with a total capacity of 320 MW. Pakistan, Nepal, Malaysia and Angola have high hydropower potential and may become priority countries for Chinese hydropower investments, seeing as they fall under the Belt and Road Initiative, a regional economic cooperation program China is heavily pushing.

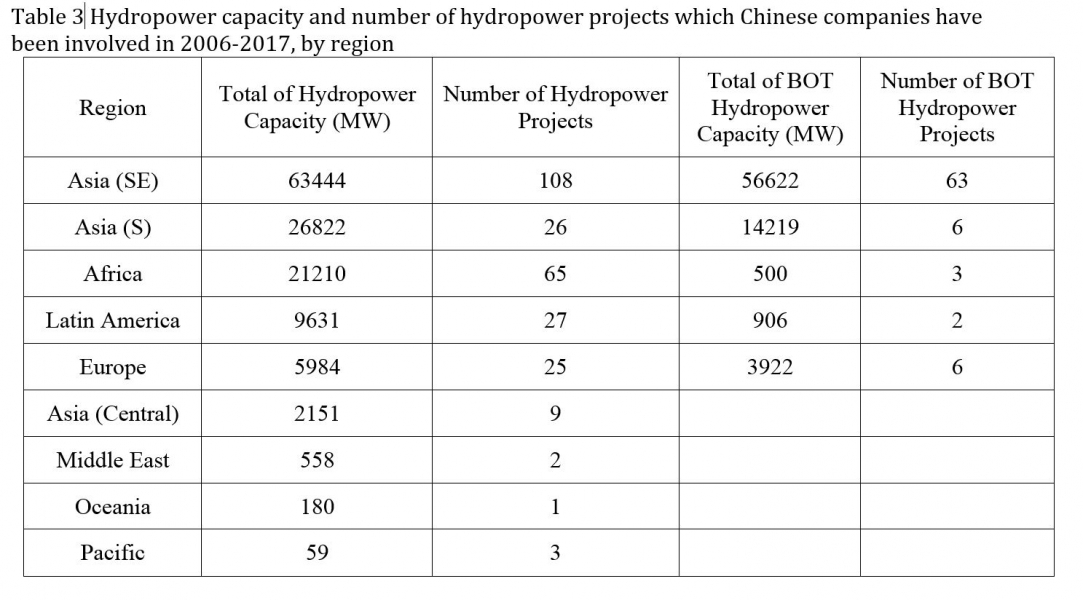

Geographic proximity, close political relationships and cultural similarities have meant that Chinese companies have had the most success investing in Southeast Asia (Table 3). Chinese companies are developing the greatest number of their projects in Southeast Asia (41%), representing 49% of megawatt capacity. BOT projects are most common in Southeast Asia, where 74% of the projects by capacity are BOT; 79% of the total number of Southeast Asian projects are BOT.

The African continent contains the next largest concentration of projects by number, followed by Latin America, South Asia and Europe.

Because South Asia has more mega-hydropower projects, South Asia is ranked the second by capacity. In fact, in the past year, Chinese companies have had the most success in South Asia. In May 2017, China and Pakistan signed a memorandum of understanding for the Indus River Cascade including Diamer-Bhasha (4,500 MW), Patan (2,400 MW), Thakot (4,000 MW), Bunji (7,100 MW) and Dasu (2,160 MW).

Projects in Pakistan and Nepal have been revitalized and propelled with political support and new financial resources since the Belt and Road Initiative in 2015. Note that in November 2017, the status of hydropower projects in both Pakistan (Diamer-Bhasha) and Nepal (Budhi Gandaki) was contested.

Some of the projects which are currently under consideration are not new projects. For example, the Kohala hydropower project contract was first awarded to CWE in 2011, the Bunji was awarded to CTG in 2009, and the West Seti project was given to China International Water & Electric Corporation in 2012.

In Latin America, Chinese companies have been most active in Bolivia, Ecuador and Honduras, and are presumably looking to have a bigger market share in the top six countries by installed hydropower capacity — Brazil, Venezuela, Colombia, Argentina, Paraguay and Chile (from 2015 Hydropower Status Report). The greatest business expansion for Chinese hydropower companies in Latin America occurred in 2011, and Chinese companies haven’t had much success in securing new contracts since. Perhaps this is because Latin American countries require much higher standards and represent significantly higher political risks. The higher laws and standards in the host countries not only lead to higher financial costs and greater technical challenges, but also present higher legal risks to the Chinese companies. For example, the Nestor Kirchner and Jorge Cepernic hydropower projects that Gezhouba won in 2013 in Argentina were subsequently suspended by the Supreme Court in 2016 because the federal government didn’t perform mandatory studies and consultations.

The Most Influential Chinese Hydropower Companies

The first five companies listed here are State-Owned Enterprises (SOE). The current Chinese administration is endeavoring to make further reforms to SOEs, which have already dramatically evolved since the early ‘70s.

1. PowerChina Resources and Sinohydro have merged and are now wholly owned by Power Construction Corporation of China. Sinohydro is mainly a project contractor, undertaking EPC and other construction contracts, while PowerChina Resources focuses on construction and operation, undertaking BOT contracts in other countries. During the ten-year period reviewed, Sinohydro comes out as the Chinese company that has built the most hydropower capacity (48,828 MW) and largest number of hydropower projects (118 projects). For 28 of these projects, Sinohydro collaborated with Chinese BOT developers. That said, the number of hydropower projects signed by Sinohydro decreased after 2013. According to 2015 and 2016 annual reports published by PowerChina, the contribution of income from Sinohydro’s hydropower construction business (both domestic and overseas) to the overall income from its building and construction business experienced a continuous decrease between 2013-2016, and dropped from 44% in 2013 to 28% in 2016 (from 2015 PowerChina Annual Report and 2016 PowerChina Annual Report). At this point we do not know whether Sinohydro has adjusted its strategies, and whether it is looking into new geographical areas, or new industry areas. PowerChina Resources is involved in BOT projects. It completed Kamchay (193 MW) in Cambodia, and now is building the Nam Ou Cascade (1,156 MW) in Laos and Busanga project (240 MW) in the Democratic Republic of Congo. Projects in the pipeline for PowerChina Resources include Lower Sesan 3 in Cambodia, Pak Lay in Laos, and Lasolo in Indonesia.

2. China Gezhouba Group Corporation is a member of China Energy Engineering Group Co., Ltd. Gezhouba was founded in 2006 and is a major hydropower project contractor in China that has mainly undertaken EPC contracts or other construction contracts. Gezhouba is second to Sinohydro in terms of its overseas hydropower development. It has a total hydropower capacity of 30,409 MW and 42 completed projects. Gezhouba has experienced a drop in overseas projects between 2012-2015, but has gained growth again in the last two years, thanks to projects repackaged under the Belt and Road Initiative.

3. China Three Gorges Corporation (CTG) is the third largest hydropower entity. It specializes in large-scale hydropower development and operation and mainly targets large-scale BOT projects in the overseas market. China International Water & Electric Corporation (CWE) is a wholly-owned subsidiary of CTG and undertakes both BOT and EPC hydropower projects. CTG has signed 12 BOT projects and 1 EPC project under the brand of CTG with a total capacity of 27,066 MW. The BOT projects CTG have signed are all mega projects, and located in Pakistan, Burma, Nepal and Russia. To date, only the Karot project (720 MW) in Pakistan has begun construction. In addition to the projects signed under the brand of CTG, its subsidiary, CWE, has signed 6 BOT projects and 29 EPC projects with a total capacity of 5,351 MW.

4. China Power Investment Corporation (CPI) was a state-owned electricity producer and is now known as the developer of the (suspended) Myitsone mega Dam (6,000MW). In 2015, CPI merged with the State Nuclear Power Technology Corporation to become State Power Investment Corporation (SPIC) which is one of the five biggest power generation enterprises in China. All the projects CPI has signed have been BOT, located in Burma and to date have not had any progress.

5. China Guodian Corporation (Guodian) is also one of the five biggest power generation enterprises in China. Guodian operates power generation plants- mainly thermal power, hydropower and wind power. Earlier in 2017, Guodian merged with Shenhua Group Corp., China’s top coal miner. This new entity has assets of USD $271 billion, and will be the world’s second-biggest company by revenue and largest by installed capacity and the new entity will be moving towards increasing renewable energy solutions rather than coal. Guodian has signed three BOT projects, Nam Tabak and Mawlaik in Burma, and Sambor in Cambodia (recent news indicates that Guodian may have withidrawn from Sambor and that Huaneng has taken over).

6. China Datang Corporation (Datang) was founded in 2002 and is also one of the five biggest power generation enterprises in China. Datang’s projects are BOT and are mainly located in Burma, Cambodia and Laos. The completed projects are Dapein 1 in Burma, and Stung Atay in Cambodia. The Pak Beng and Sanakham in Laos are under consideration.

7. Lastly, China National Electric Engineering CO., Ltd (CNEEC) is a state-owned professional international engineering company. Its overseas focus has been EPC contracts and other construction contracts. CNEEC has been involved in the construction of 12 hydropower projects. CNEEC undertakes relatively small projects (<100MW), but its geographical footprint covers most regions of the globe.

Conclusion

In considering what might lie ahead for Chinese overseas investments in the hydropower sector, it is useful to remember where China stands at the end of 2017. During the 19th Party Congress which concluded on October 24th, Xi Jinping, the General Secretary of the Communist Party of China and President of the country, declared the coming years as a time for the Chinese nation to transform itself into “a mighty force” to lead the world on political, economic, military and environmental issues. The Communist Party of China believes that between now and 2050, will be “an era that sees China moving closer to centre stage and making greater contributions to mankind.” We can expect that China will become an even greater role model for developing countries. Knowledge and understanding of China’s behavior overseas may also help to predict ambitions and trends of other nations.

Xi aspires to make the Chinese nation and the Chinese Communist Party strong, both domestically and on the world stage. Through his signature policies such as the Belt and Road Initiative and bilateral and multilateral economic agreements between China and other nations, and with recently established and well-funded financial institutions ready to back overseas projects, it is likely that Chinese overseas investments in many sectors, including hydropower, will grow exponentially.

Chinese power corporations are increasingly assertive and comfortable with their overseas roles as developers and contractors. Many have realized that their overseas projects are more successfully implemented when they engage with and listen to the advice from non-governmental organizations. NGOs are able to gather more nuanced information about social and environmental concerns on the ground. We can expect that the savvier corporations will prioritize better engagement with Chinese and foreign NGOs in the countries where they are building projects.

If you have comments, questions about our China global work, or information which should be included in this dams database, please contact Stephanie Jensen-Cormier (sjcormierATinternationalrivers.org).

Recent Posts in Blog

- China shows its commitment to protecting domestic rivers, cultural heritage - July 11, 2018

- China Commits to Protecting the Yangtze River - February 26, 2018

- Reflections on Chinese Companies’ Global Investments in the Hydropower Sector Between 2006-2017 - December 14, 2017

- The Most Endangered Turtle in the World - September 13, 2017

- Health and Happiness for China’s Rivers in 2017 - January 11, 2017

Image Gallery